Stop Funding the 'Average' Consumer. They Don't Exist.

- uzmakrauf

- Jun 4

- 7 min read

Ask your team to describe your target consumer and you’ll hear the same profile:

35–54, Household income in the low six figures, quality-conscious, values convenience, shops omnichannel.

She shows up in every briefing deck. She shapes your media plan.

And she’s one of the reasons your ROI is under pressure.

Because she’s not a real person.

She’s an average – built by blending different generations, ethnicities, and income levels, each with fundamentally distinct needs, behaviors, and values.

Further, the consumer herself is under pressure. And it shows in the numbers:

While the US GDP forecast of +2.5% for 2026 suggests a story of stability; It isn't:

That growth is driven almost entirely by business investment in AI infrastructure and labor market stabilization (Goldman Sachs).

Meanwhile consumer-based consumption – which drives two-thirds of the economy – is growing at just 1.6–1.9% as consumers pull back (Deloitte).

Brands now face two compounding consumer challenges: increasing fragmentation and increasing consumer scrutiny on every dollar they spend.

Without understanding and catering to real consumer segments, brands will fail in an already tight market.

Here’s where most brands lack clarity on their consumer:

1. Consumer Bifurcation:

Growing K-shaped divergence in purchasing power:

The Upper Income growth: The top 20% of US households hold 72% of US wealth, and are driving growth. They are largely immune to rate hikes, shielded by high interest income and locked-in low mortgage rates. Their spending is more robust – growing at 2.6% YoY – fueling demand for premium electronics and experiential travel (Fox Business)

The Lower Income decline: The bottom 60% hold just 15% of all wealth, and face severe financial constraints. With costs of essentials up ~25% over five years, their discretionary spending has effectively hit a ceiling. For this majority, 'Value' is a financial necessity. (Fox Business)

2. Changing Definition of Value:

Consumers don't equate "value" with "cheap."

It has now evolved into a complex calculation of Quality + Experience + Price that consumers scrutinize for every purchase, be it a $5 snack or a $2,000 appliance.

And this lens of “is it worth it?” is applied by all income levels of consumers, not just lower.

Brands that rely on their heritage or "premium" labels without delivering tangible quality are being filtered out. As McKinsey data above shows, a consumer’s perception of Quality (72%) has overtaken Price (70%) as the primary driver of purchase decisions in 2025 [McKinsey].

Deloitte research finds that 47% of global consumers are now active value-seekers, willing to sacrifice convenience for cost-conscious or deal-driven choices [Deloitte].

3. "Trading Down to Trade-Up":

Financial pressure is no longer confined to lower-income tiers.

Nearly 35% of high-income households now identify as "value seekers" [Deloitte].

We see significant behavioral shift where affluent consumers are switching to private label essentials (like Costco's Kirkland) to preserve budget for specific "splurges" like clinical skincare or experiential travel.

This is where brand margin erodes – consumers trade down on your core SKUs to fund someone else’s premium.

4. Generational Divergence:

Each age cohort, gender and race has distinct needs, values, expectations, and wealth.

You cannot successfully operationalize one plan across them.

Cohort | Key Behavioral Driver 2026 | Spending Priority | Strategic Implication |

Co-Creation & Visual Aesthetic | Snacks, Digital Goods, Skin-care | While they lack direct credit, they influence a significant portion of household discretionary spend. They demand "Zero-friction" speed and interactive, aesthetic-first brands that prioritize real-world credibility over polished ads. | |

Gen Z (Digital Natives) (20% of US Pop) | Identity & Authenticity | Experiences, Wellness, "Dupe" Culture | This cohort is hugely influential and distrusts polished marketing, relying on social search for discovery. They demand "raw" authenticity and are willing to switch brands instantly for better alignment with values or price. They fuel the "dupe" economy, prioritizing efficacy over heritage. [Circana] |

Millennials (The Squeezed Middle) (22% of US Pop) | Convenience & Hybridity | Family essentials, Hybrid retail | Now in peak earning (and spending) years, they are the "Squeezed Middle" balancing childcare and careers. They demand "Phygital" efficiency (e.g., BOPIS) to save time and celebrate "minorstones" to validate their hard work. [Porch]. |

Gen X (The Overlooked Powerhouse) (19% of US Pop) | Pragmatism & Efficiency | Functional upgrades, Value longevity | Often overlooked, Gen X prioritizes durability and efficiency. Caring for both children and aging parents, they focus on stress reduction and products that simplify household management. [Porch]. |

Boomers (The Wealth Holders) (21% of US Pop) | Health & Stability | Healthcare, Travel, Premium consumables | Controlling 40% of national assets, Boomers are less price-sensitive regarding health and wellness. They prefer clear navigation, loyalty programs, and "white glove" service over AI chatbots. [Circana] |

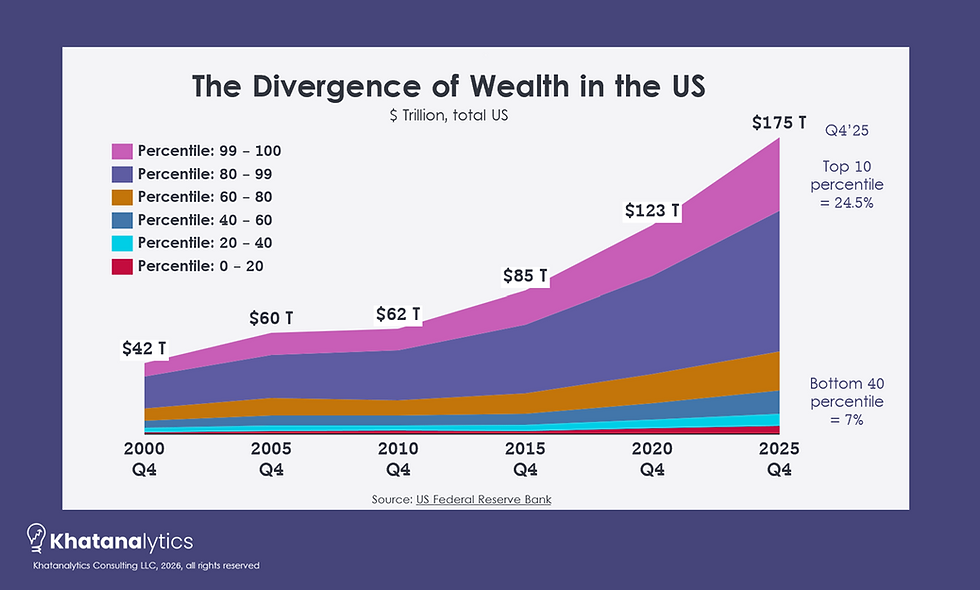

5. The Wealth Divide:

Gen Z is a powerful cultural engine and a future growth driver.

But they aren't where today’s profit sits.

As of Q4 2025, US wealth is extremely concentrated by age:

consumers over 55 own 74% of total US wealth ($129 Trillion of the $175T total),

while those under 40 own just 7% ($11.5T).

While a significant "Great Wealth Transfer" via inheritance will eventually boost Millennial and Gen Z financial health, the current reality is a polarized market.

That creates a structural tension most strategies fail to resolve.

You need Gen Z to drive relevance, discovery, and cultural momentum.

But you need older, asset-heavy consumers to drive revenue, margin, and stability.

Most plans blur this distinction – they are over-indexed on influence, as they chase younger consumers, but under-indexed on monetization, by ignoring older ones.

Winning brands separate the two roles clearly. They build for influence and for monetization – on purpose, with different strategies, different channels, and different expectations of return.

Implications: What this may be costing you right now

When budget flows to the “average” consumer, three things happen:

Your premium tier gets under-funded because the composite doesn't demand it.

Your value tier gets under-funded because the composite can "afford" the middle.

Your market share gets shifted to insurgents, private label, and premium niches – none of which your plan thought it needed to defend.

Plus, the compounding cost: Your retailer buyer sees a brand that doesn’t know its shopper or their trip missions resulting in weaker JBP outcomes, feature support and store space.

Four questions to pressure-test

If any of this feels uncomfortably familiar, four diagnostics will clarify where your plan may need working.

The Middle-Market Trap: Are your core products too expensive to be the trade-down essential, but not distinct enough to be the trade-up splurge? If yes, your growth depends on one of those positions strengthening – not on the middle recovering.

The Occasion Audit: You know who buys your product. Do you know why? If your calendar is still built around traditional holidays, you're missing the high-frequency Minorstones driving growth in snacking, beauty, and affordable premium.

The Worth-It Test: In a savings-rebuild cycle, every purchase demands a higher threshold of justification. Does your messaging emphasize durability, efficiency, and specific quality signals strongly enough to unlock the wallet of a consumer who is actively trying not to spend? If your pitch is heritage, you're relying on a driver the market has already moved past.

The Brand Equity Test: Data shows 'Quality' has surpassed 'Price' as the #1 driver. If you stripped your logo off the package, would the consumer objectively rate your product superior to the private label sitting next to it? If not, your premium pricing is at risk.

Answered honestly, these surface why deep clarity on your consumers is critical to building strategies that actually work.

What winning looks like

The brands pulling ahead aren’t building more personas. They’re making sharper decisions.

They replace the “average consumer” with a small number of high-conviction segments – defined by current values, preferences and behavior, not just demographics – and use them to define where they play and how they win.

Instead of one integrated plan designed to work for everyone, they run distinct investment cases tied to specific consumer needs, portfolio roles, and outcomes.

And they fund them differently.

Spend shifts away from broad-reach efficiency toward focused cohort strategies – different media, different retail execution, different creative, and different KPIs.

It is more complex. But it is also why some brands are growing while others are optimizing strategies that were never aligned with how growth actually happens now.

This is where we work

Khatanalytics helps brands close the gap between how they think about consumers and shoppers – and how they actually behave.

We build clarity in consumer understanding, segmentation, and retailer alignment – so brands can move from broad assumptions to high-conviction decisions on where to play, how to invest, and how to show up at retail.

Because many brand strategies are still structurally misaligned with how growth actually happens now.

Understand where your current consumer model falls short – and what it will take to fix it.

The perspectives in this blog draw from Khatanalytics’ 2026 Macro Trends research report, covering how consumer divergence, retail power shifts, and AI-driven discovery are reshaping category growth. Access the full report:

About the author

Uzma Khatana Rauf is the founder of Khatanalytics, a marketing intelligence and strategy consultancy specializing in Consumer & Shopper Experience Journey (CEJ) intelligence.

A former VP of Consumer, Shopper & Market Insights at Samsung, Head of Shopper Insights at Unilever, and VP of Custom Analytics at Nielsen, she helps mid-to-large CPG and Consumer Electronics brands develop higher-ROI strategies by knowing precisely where to invest across the full consumer journey.

Contact: uzmarauf@khatanalytics.com

FAQs

Q1: Why is targeting the "average consumer" a problem for CPG and Consumer Electronics brands?

The average is a statistical blend of generations, income tiers, and life stages with very different needs. Funding the composite under-resources both your premium tier and your value tier, leaving share open to insurgents and private label.

Q2: What is K-shaped consumer divergence?

K-shaped divergence describes the widening gap between upper-income households, who continue to spend at roughly 2.6% growth, and the bottom 60%, whose discretionary spend has effectively flatlined as essentials have risen ~25% over five years. The two groups now behave like separate markets.

Q3: How should brands segment consumers in 2026 instead?

Replace persona averages with a small number of high-conviction segments defined by current behavior – not demographics – and fund them with distinct media, retail execution, creative, and KPIs. Separate the role of "influence" cohorts from "monetization" cohorts on purpose.

Comments